Super Contributions: Use it or Lose it

If your superannuation account balance was less than $500,000 as at 30 June 2025, you have until 30 June 2026 to catch up any unused concessional superannuation contributions from 2021.

From the 2020 financial year onwards, new rules came into effect that enabled individuals with a total superannuation balance of less than $500,000 to catch up on superannuation contributions that may not have been maximised made in prior years.

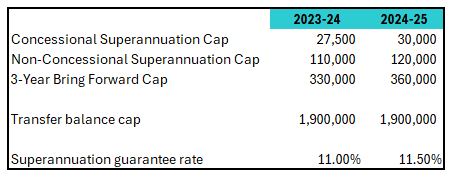

For example, in the 2021 year, the total concessional contribution cap was $25,000. If you only made contributions of $15,000, then you have $10,000 unused from that same year. You can carry this unused cap balance forward for up to 5 years. After 5 years, the unused balance expires. This means that you have until 30 June 2026 to use up any unused concessional cap from the 2021 financial year. If you don’t use up the 2021 carried forward balance before 30 June 2026, it will be lost.

But there’s a catch: your current year contributions first go towards this year’s cap ($30,000). Once you have maximised your contributions for the current year ($30,000), any additional concessional contributions go towards your prior year caps, starting with the oldest.

So, to claim your 2021 unused cap, you’ve first got to contribute your full 2026 concessional contributions cap ($30,000). Anything above that goes towards your unused caps from previous years, starting with 2021.

Not sure what your prior year unused caps are? You can check your myGov ATO account. Alternatively, if you are on our tax agent’s list we can also access this information.

Now, before proceeding, we recommend that you chat with your financial planner to make sure the additional contributions align with your retirement goals.

Remember, if you are looking to claim a personal tax deduction for superannuation contributions, you need to:

- Ensure the contribution is received by your superfund prior to 30 June 2026;

- Give your superannuation fund a “Notice of Intention to Claim a Tax Deduction” for the contributions;

- Receive an acknowledgement letter from your fund prior to lodging your 2026 tax return.

DISCLAIMER: The information in this article is general in nature and is not a substitute for professional advice. Accordingly, neither TJN Accountants nor any member or employee of TJN Accountants accepts any responsibility for any loss, however caused, as a result of reliance on this general information. We recommend that our formal advice be sought before acting in any of the areas. The article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our consent,

Jeanette has over 20 years experience as an accountant in public practice. She is a Chartered Accountant, registered tax agent and accredited SMSF Association advisor. When she is not helping business owners grow their empires, you will likely find her out running on the trails or at the gym. Book in to see Jeanette today.