Last night Federal Treasurer Scott Morrison handed down his third budget. While there were no shocks or great surprises in the announcements, there were some welcome tax reform measures.

A shared feeling among most budget commentators is that this was a “victimless” budget – that is, no one particular group suffered from the announcements.

So what did we like in the Budget? Individual taxpayers will appreciate tax cuts via a low and middle income tax offset and the changes to the tax brackets. Small businesses will get an advantage from the extension of the $20,000 instant asset write-off (and the proposed reduction to the company tax rate as announced in previous Budgets). Retirees have not had any significant changes made to superannuation – which is a welcome change for an industry still trying to come to grips with the superannuation changes made from previous budgets. Scott Morrison also confirmed that the Government will not be making any changes to the current franking credit regime (we await the opposition’s Budget response to see if they will continue with their suggested changes to franking credits).

The tax changes proposed in last night’s Budget will now become part of the upcoming federal election battleground. We hope that the proposed cuts to the company tax rate and the removal of the 37% individual tax bracket will be high on the Government’s agenda.

We’ve outlined below some of the main tax and other business measures that were announced in the Budget.

As with all budgetary measures, these measures are not final until the relevant legislation has been passed by the Government. As such, it is important that you use caution in acting on these measures until they have become law. We will keep you updated on the status of these proposed measures.

Businesses

-

Instant Asset Write-off – The $20,000 instant asset write-off for small businesses (who have an aggregated annual turnover less than $10 million) has been extended to 30 June 2019. Assets acquired for more than $20,000 will be pooled and depreciated at 15% in the first year then 30% each year thereafter. The balance of this pool can be written off when it is less than $20,000.

-

Taxable Payments Annual Reporting System – From 1 July 2019, the taxable payments annual reporting system to be expanded to the following industries:

-

Security providers

-

Investigation services

-

Road freight transport

-

Computer system design and related services.

-

The taxable payments annual reporting system already applies to the building industry and will extend to the cleaning and courier industries from 1 July 2018.

-

Non-compliant payments – From 1 July 2019, businesses will not be able to claim deductions for payments to their employees, such as wages, where they have not withheld any amount of PAYG from the payments, despite the PAYG withholding requirements applying.

-

Non-compliant payments – From 1 July 2019, businesses will not be able to claim deductions for payments to contractors where the contractor does not provide an ABN and the business does not withhold any amount of PAYG despite the withholding requirements applying.

-

Director Penalty Notices – Currently, under the Director Penalty Regime, the ATO can make directors personally liable for superannuation and PAYG withholding. The Director Penalty Regime is set to extend to GST, luxury car tax and wine equalisation tax potentially making directors personally liable for these debts also.

-

Corporate Tax Cuts – The Government is committed to its Ten Year Enterprise Tax Plan of company tax cuts announced in the 2016-17 Federal Budget (which will see the corporate tax rate cut to 25% for all companies by 2026-27).

Individuals

-

Medicare Care Levy –

-

The Medicare levy low-income thresholds increased from the 2017-18 income year.

-

The Medicare levy rate will remain at 2%. The Medicare levy rate was previously budgeted to increase to 2.5% to pay for the NDIS. However, the Government has been able to fund the NDIS through the budget without increasing the Medicare levy.

-

-

Seven year personal income tax plan –

-

Step one – Tax Offset: A low and middle income tax offset will apply from 1 July 2018 to 30 June 2022. The offset will give taxpayers up to an extra $530 of their tax back if they earn less than $90,000. The offset then reduces and is completely phased out at $125,333 taxable income. This offset will exist in addition to the Low Income Tax Offset.

-

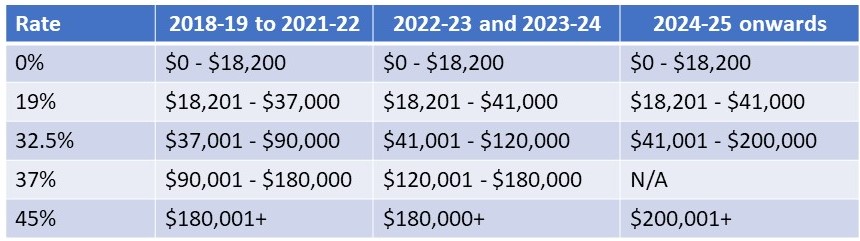

Step two – Tax Rates: Individual tax brackets are being changed to prevent more Australians from moving into higher tax brackets. See the table of the new tax rates below.

-

Step three – Simpler System: The personal tax system will be simplified by removing the 37% tax bracket entirely from 1 July 2024. The highest marginal rate of 45% will apply to taxable income exceeding $200,000. A summary table of the new tax rates is below:

-

Superannuation

-

Protecting Your Super – From 1 July 2019, the Government will ban exit fees on all superannuation accounts. This gives superannuation members greater flexibility to change funds.

-

Protecting Your Super – From 1 July 2019, the Government will introduce a 3% annual cap on passive fees charged by superannuation funds on accounts with balances below $6,000.

-

Protecting Your Super – From 1 July 2019, all inactive superannuation accounts with a balance less than $6,00 will be transferred to the ATO. The ATO will use data matching to reunite these funds with the member’s active accounts, where possible.

-

Insurance – From 1 July 2019, insurance will be offered on an “opt-in” basis to superannuation members with balances of less than $6,000, members under 25 years of age or members who have not made a contribution for 13 months and are inactive.

-

Work test exemption – From 1 July 2019, the Government will introduce an exemption from the work test for voluntary contributions to super for people aged between 65-74 with superannuation balances below $300,000 in the first year that they do not meet the work test.

-

SMSF – The maximum number of members for self-managed superannuation funds will increase from 4 to 6 from 1 July 2019. This will give SMSFs greater flexibility and allow for better succession planning for larger families.

-

SMSF – A 3 yearly audit cycle will be introduced for SMSFs from 1 July 2019 for funds that have a history of 3 consecutive years of clear audit reports and have lodged the fund’s annual returns in a timely manner.

Research and development

-

The R&D tax incentive is to be amended to improve its integrity. The proposed changes will apply from 1 July 2018. The R&D tax offset will be 13.5% above the claimant company’s tax rate. Further, there will be a cap of $4 million per annum for the cash refunds from the R&D tax offset.

We will keep you up-to-date with the progress of the implementation of these proposed measures.

If you would like to discuss the tax implications of the budget proposals, please call us on (07) 56656469.

DISCLAIMER: The information in this article is general in nature and is not a substitute for professional advice. Accordingly, neither TJN Accountants nor any member or employee of TJN Accountants accepts any responsibility for any loss, however caused, as a result of reliance on this general information. We recommend that our formal advice be sought before acting in any of the areas. The article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our consent,

Jeanette has over 20 years experience as an accountant in public practice. She is a Chartered Accountant, registered tax agent and accredited SMSF Association advisor. When she is not helping business owners grow their empires, you will likely find her out running on the trails or at the gym. Book in to see Jeanette today.